The reality check ahead for YOLO generation

News

|

Posted 08/12/2022

|

17943

It seems YOLO (you only live once) is at large in so many ways right now. We’ve spoken to the so called “Great Resignation” and Quiet Quitting in the US and here, and China’s “Lying Flat” movement as well where people, young in particular, are completely disillusioned with the socioeconomic disconnect in the world and new found love of working from home still being tolerated (for now). There appears a growing sense that economic prudence is old school and reckless abandon is in. Unfortunately it appears governments too often have a similar mindset…

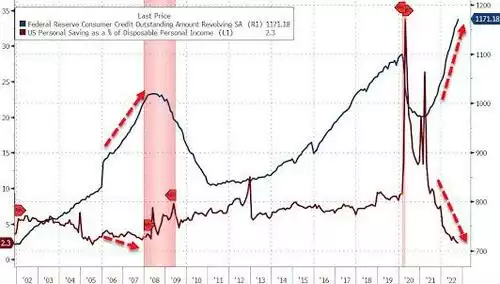

Please consider exhibit A below fresh out of the US last night. Credit card debt has hit an ALL-TIME high whilst savings have hit a 17 year low! If ever we saw an ‘alligator trap’…

The correlation between such a disconnect and ensuing recession is pretty clear. After a decade of easy money we have an entire generation not familiar with the concept of non near zero interest rates and the debt servicing consequences of that. To be fair in Australia our own RBA was telling them it would stay that way until at least 2024! Apart from the very short and sharp recession of COVID, this generation in Australia hasn’t seen a proper recession in decades as COVID was so short and sharp and China saved us from the full impacts of the GFC. It’s a generation without economic consequences.

The chart above tells a very clear story of both a society unable to keep up with inflation as it far outpaces wage growth AND the YOLO crowd happy to live beyond their means, as never before have there been the consequences as before them now. We talked about the wage piece at length this week both here and also in the Insights interview with Alex Hutchinson here.

In Australia we also have a generation that has never seen material pressure on home loan interest rates combined with inflation, nor a property market that does anything but go up. Betting the house took on new meaning. That is about to change. From Macro Business yesterday:

“CoreLogic’s Eliza Owen tipped an increase in forced property sales in 2023 once hundreds of billions of dollars worth of fixed rate mortgages roll over from their current cheap emergency low interest rates (circa 2%) to 5% or 6%.

“While the majority of home owners will still be able to service their loans, we could see a bit of additional supply hitting the market as people need to sell. This would presumably put further downward pressure on prices”, Owen said.

Her view was supported by AMP Capital’s chief economist, Shane Oliver.

“I think there’s more pain ahead of us, and until the RBA cuts interest rates, and we’ve seen the worst of the fixed mortgage reset, I think there’s more downside in prices all the way up to the September quarter next year”, Oliver said.

“I think we’re going to see some pick up in distressed sales as a result of ongoing rate rises at a time when a large number of mortgage holders are coming off their record-low fixed loans”.

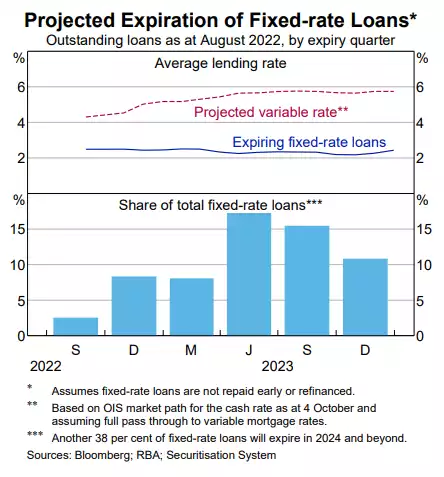

The latest Financial Stability Review (FSR) from the Reserve Bank of Australia (RBA) noted that “around 35% of outstanding housing credit is on fixed-rate terms” and “around two-thirds of these loans are due to expire by the end of 2023” (see next chart).

The RBA estimates that “most fixed-rate borrowers with loans expiring in 2023 will face discrete increases in their interest rates of 3–4 percentage points when they roll over to variable rates”, and that “almost 60% of borrowers with fixed-rate loans would face an increase in their minimum payments of at least 40% when they expire”.

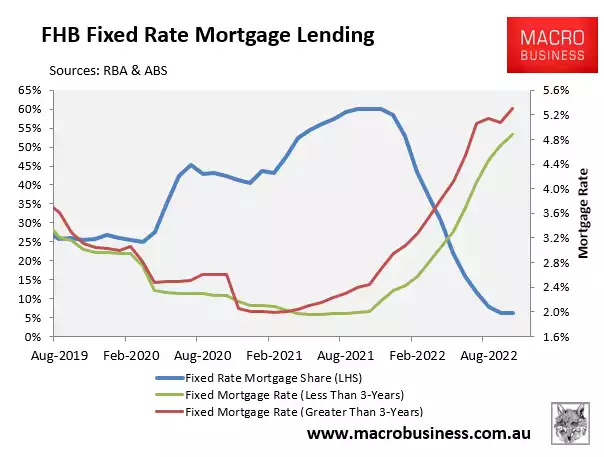

First home buyers (FHB) dominated fixed rate mortgage lending over the pandemic (see next chart) and are most exposed given they “tend to enter the housing market with relatively high initial LVRs” and “have had less time to accumulate excess payments”.”

Yesterday’s GDP figures for Australia came in softer than expected but the key takeaway was that the bad news is ahead of us not this measure behind. The Treasurer said:

“We know that the difficult economic conditions, particularly in the global economy, are not behind us. They are ahead of us,”

Westpac was blunt in their assessment with the message of ‘Just wait until mortgages reset, house prices keep falling and consumption comes apart.’

“Key surprise: The real estate sector – in the form of Ownership Transfer Costs (turnover in the property sector) plunged by -11.2%, subtracting 0.2ppts from activity. We [Westpac] had allowed for a more modest fall (recent quarterly outcomes have been -1.1%, -2.5% and -2.1%).

This provides further evidence that the Australian economy is in transition. Earlier tailwinds are fading, and the impacts of high inflation and higher interest rates are beginning to become apparent. A sharp economic slowdown is in prospect for 2023.”

The pain ahead for Australia, and indeed the world, is that we are all focussed on backward looking metrics. The set up for the pain of these rising interest rates is all ahead and very real given the unprecedented amounts of debt in the system and a generation without the discipline borne of having been through a proper recession or the fiscal responsibility it teaches.

Unfortunately that is as true for governments as it is for individuals. Populism not prudence rules and fiscal deficit spending is the cure for all ills. It all amounts to more debt amid higher rates. The alligator jaws above apply at this level as much as the individual.

The greatest Christmas gift those who understand can do for those who don’t, is teach them about real money – gold and silver bullion.