Pakistan - The Failed State

News

|

Posted 03/02/2023

|

12941

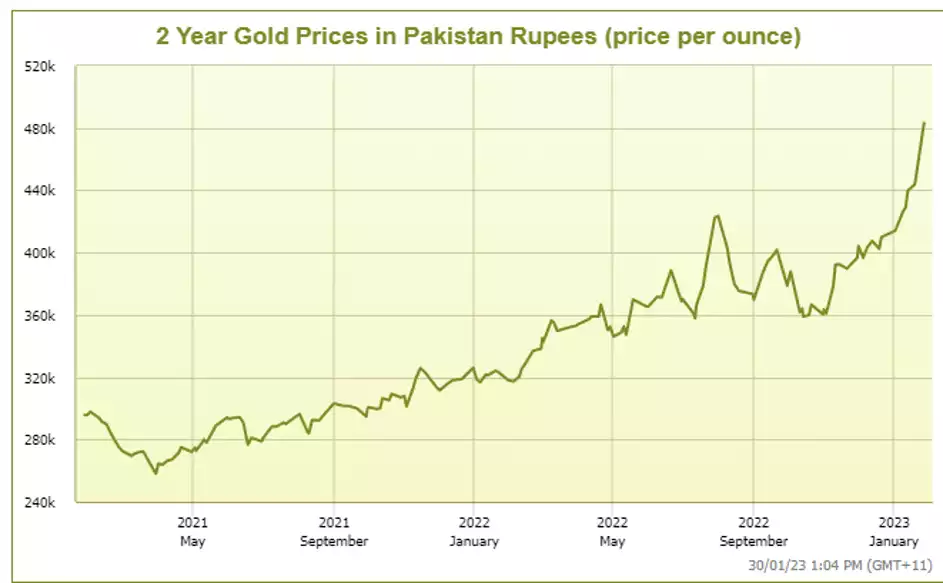

Pakistan appears to be the next domino to fall in the global currency collapse. The Pakistani Rupee has been in freefall against other fiat currencies, dropping 13.7% against the US dollar over the last couple of days. Gold is now up over the psychological barrier of RS500,000/oz, an all time high.

Waves of panic buying have been reported by jewellers across the country over the last couple of months. Word on the street in Karachi is that even at record spot prices, there are almost no buybacks taking place.

Food security is continuing to worsen as the 2022 floods have exacerbated supply issues as farmland equivalent in area to the Czech Republic (78,000 sq km) has been rendered unproductive. The damage spans 81 districts and has affected approximately 80% of the country’s agricultural resources. Shortages are pushing the country to the brink of societal collapse. Symptomatic of the rising pressures, on Jan 24th, a shopkeeper was shot dead by two men looting grain. Ousted former Prime Minister cricketing great Imran Khan, ironically, suggested that the country could celebrate Ramadan early so that the country can fast instead of going hungry due to high inflation and scarcity of food.

Previously blackouts have been fixed within a couple of hours, but the recent grid breakdowns have left Karachi, Islamabad and Lahore with no electricity. Metro stations throughout the country have been out of commission for the last couple of days. It is estimated that 90% of the population is now without power or relying on backup generators, with hospitals and airports being the main essential services with significant energy capacity. Earlier this month, in an attempt to reduce energy consumption, shopping Malls and restaurants have been ordered to close by 20:30 and 22:00 respectively.

Unfortunately, none of this comes as a surprise for those following the developments over the last year, as Pakistan is asking for $1.1bn immediately to stave off default. The installment is part of a $46bn bailout promised in 2019 from the International Monetary Fund (IMF). The IMF is sending a delegation to Islamabad from 31 January until 9th of February to try to kickstart the stalled discussions. Pakistan is now desperate to secure external funding as they now have less than three weeks’ worth of import cover in its foreign exchange reserves. This has led to a backlog of shipping containers full of imports such as raw materials, food and medical supplies. Ships are backed up at Pakistani ports as buyers are unable to pay for the deliveries.

In response to recent floods, Pakistan has asked the World Bank for $16.3bn in emergency aid to fund reconstruction, although this funding is also contingent on the subcontinental nation completing the fiscal consolidation and economic reforms demanded by the IMF.

It certainly seems that the walls are closing in fast on Pakistan. Their currency is crashing as citizens scramble to secure basic necessities and rely on backup generators for power. One group of Pakistanis that have managed to maintain their wealth, are gold holders.

According to the 17th century philosopher John Locke’s social contract theory, the state promises to preserve life, liberty and property. In a country where citizens cannot rely on the purchasing power of the currency, reliable access to food or energy, Pakistan is careening towards Failed State status.

This is also a salient reminder that Fiat currency is ‘money’ backed by the promise of the State. But without the State it’s a mere piece of plastic, paper or tin. There is no need for the mocking air quotes when one describes gold. It is real money that has survived 5000 years and many, many examples of what is happening in Pakistan right now. Every time.