Bond Markets Fracturing

News

|

Posted 28/08/2025

|

2069

Around the world bond markets are starting to fracture From Japan, with 40 months of above-target CPI (2%) leading to 30-year bond prices lifting to the highest level in 30 years. To the US, with the President interfering with the Federal Reserve – a once inconceivable occurrence – causing the US dollar to rapidly deteriorate as trust in the USD fractures while debt and bond issuance accelerate. To Australia with the NDIS lifting at a 10% per annum rate creating an uncontrollable fiscal hole government’s seem unwilling to fill due to the job creation and migration Ponzi Scheme its enabling. The question is now becoming which bond market will break first – with trust in International government debt clearly being questioned by investors with the Swiss bond market climbing at 0% yields due to their fiscal responsibility and low debt.

With so many canaries in the coal mine, the unravelling of government debt is shaping up to be the next financial crisis. So which country will lead the debt collapse, and what comes next when the government backstop goes?

Japanese Bond Market Stress – When Yield control no longer works

With Japan among the most indebted nations in the world, with debt running at a whopping 236.7% debt to GDP, the likelihood that this nation is the first to default on their debt is high. Following on from the yield curve control they implemented in 2016 to maintain 10 year bond rates at around 0%, this works in a deflationary environment, but since Covid and the rampant transitory inflation – this type of control is fracturing their bond markets lifting interest on long term debt.

By implementing yield curve control Japan created an enormous carry trade, whereby Japanese investors could sell yen and buy USD investing in high yielding stocks and multiplying their return as 0% interest was paid on the leverage. The cost was the depreciation of the yen due to this policy. If the US continues to depreciate their currency anyone caught in this trade will now see this their returns diminish as the USD buys less yen to repay the debt that is now costing more to service.

Trump Federal Reserve Intervention – when yield curve control doesn’t work

The US bond issues come from its lack of fiscal control that arguably started during the GFC with quantitative easing, which was put on steroids during Covid. Quantitative easing is similar to yield curve control: it creates money to buy bonds, but they are trying to achieve different outcomes. Yield curve control targets interest rates, while quantitative easing is aimed at the stock of money in the economy. Both cause the same inflationary pressure, which in a deflationary environment like the GFC works well, but then, like addicts, governments and people became hooked on these sugar hits and have not been able to get off the train as inflation continued to rip through the world.

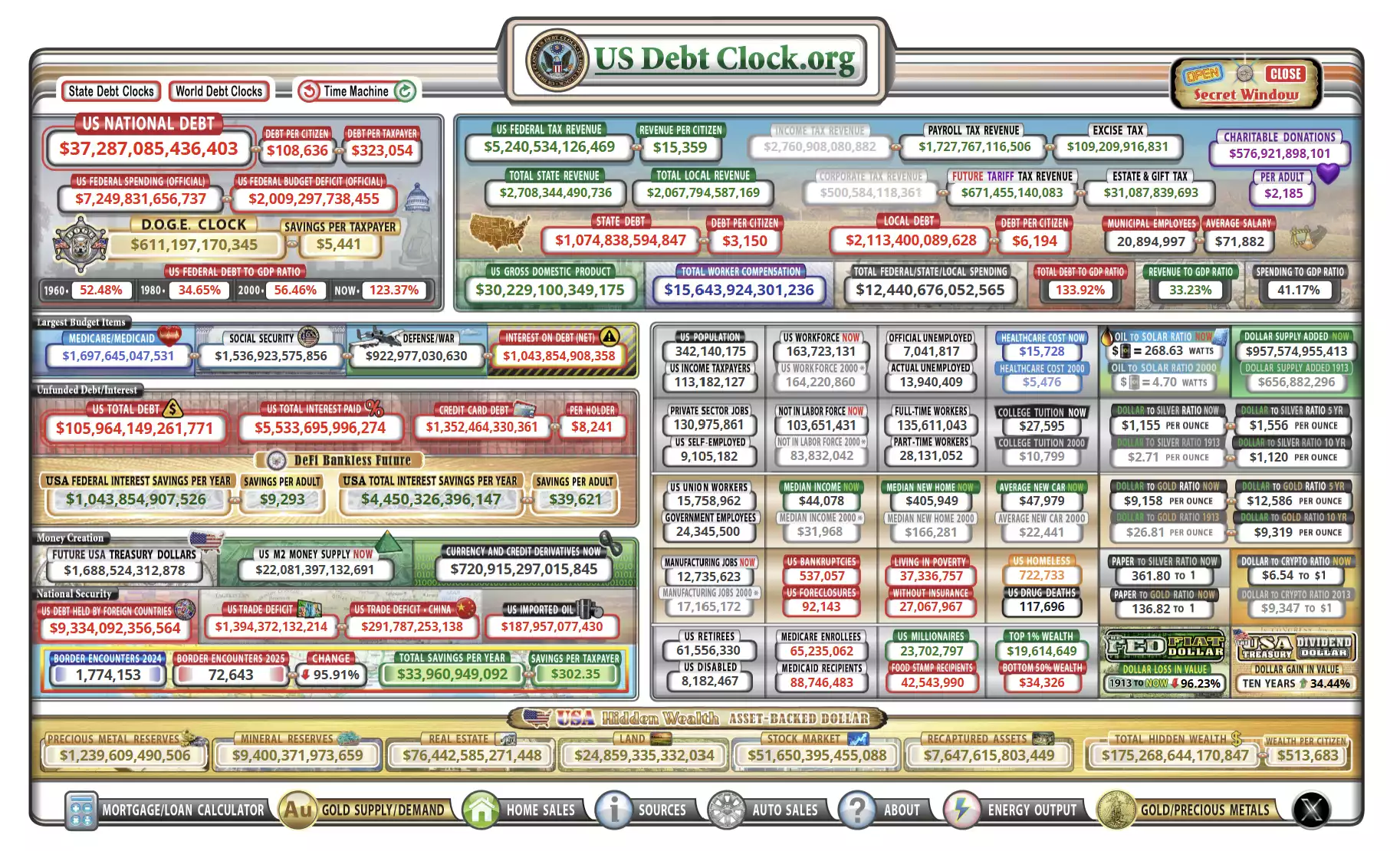

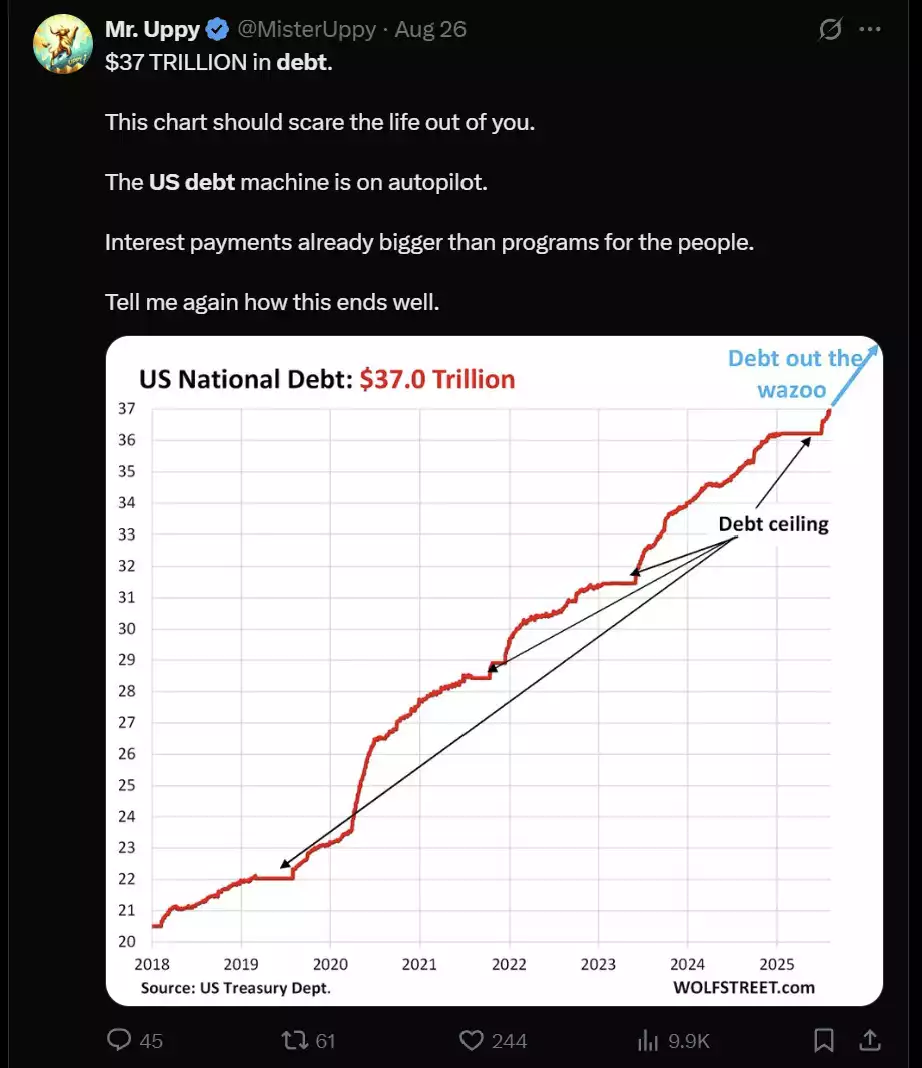

Since 2021 the US debt-to-GDP ratio has climbed from around 100% in 2019 to 124% in 2024. During the same time debt has gone from $23 trillion to $37 trillion, with $1.6 trillion being added this year alone. This has sent bond markets into a spin as US debt issuance reaches all-time highs, which under normal circumstances would lead to increased inflation and increased interest rates to cool the economy.

The Federal Reserve that sets rates, like the RBA in Australia, is used as an ‘independent’ beating stick for the government if they let the economy run too hot. But with Trump looking to ‘stack the Federal Reserve’ by ousting Lisa Cook on a mortgage fraud charge, after his recent appointment of Stephen Miran, he is hoping to help control rates by introducing another dovish committee member to reduce rates, therefore reducing interest rates payable by the US government. This lack of independence threatens the US debt market and investor confidence in it.

Funnily enough you can blame Trump all you want, but after his New York prosecution against charges of mortgage fraud, it is clear to see the Democrat weaponisation of the legal system in the US has taught him ‘to fish’, making politics much dirtier than ever.

Cooking the books with Migration - Australia

Australia, like the UK and Europe, has taken a different path by trying to cook the books with excess migration, leading to a growing welfare base, which has added to debt but not GDP, with Australia’s GDP per capita in a downward trend. To help cook the books further, additional welfare programs including the NDIS have avoided unemployment declines with nearly 1 million migrants filling government jobs with the creation of only 54,000 private jobs in 2024. In 2019 our debt-to-GDP sat around 19% and since then has grown to a whopping 43%. Unlike the US and Japan, our bond markets are not in a seeming death spiral, but our rate of increase outstrips both of them, meaning it won’t be long until we catch up. Australia’s bond market will be under threat due to the fast growth of deficits, with S&P recently stating that Australia’s AAA rating may be under threat due to lack of controlled spending and larger and larger deficits, criticising the Australian government and State governments. S&P goes on to estimate that the state budgets may hit triple that of 2019, less than 10 years from Covid.

Switzerland – why debt matters

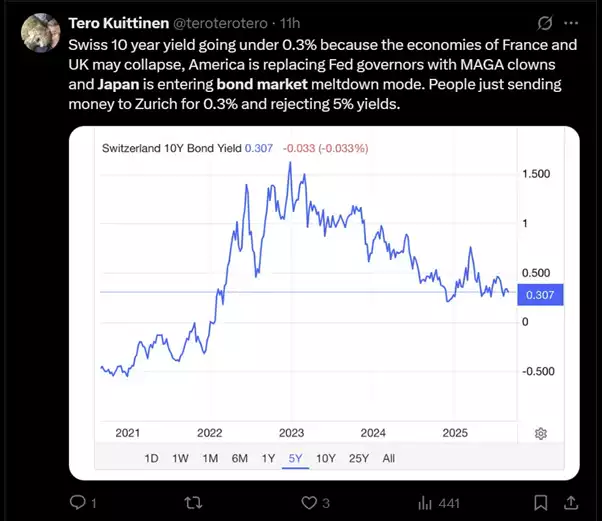

As we have previously spoken about, Switzerland is in a league of its own in regard to fiscal management. Maintaining a close to even budget year after year due to its 2003 legislated ‘Debt brake,’ right now their bond market is getting more bids than anywhere else, with investors happy to park their money in Switzerland for near 0% interest rates compared to Japan’s 30-year; 3.1%, Australia 5.0% and the US 4.9%. When investors sacrifice return for safety, there has to be something wrong.

Watch the insights video based on this article here - https://www.youtube.com/watch?v=fXD2q1Sn2kA